This economic reality highlights the importance of China’s dictum ‘seek truth from facts’. It is also crucial for China’s practical economic policy as it seeks to achieve its goal of a ‘moderately prosperous society’ by 2020 and a ‘high income economy’ by World Bank standards shortly thereafter.

But the facts of this global economic trend are also crucial for economic theory and analysis. According to the dogmas of ‘neo-liberalism’ and the ‘Washington Consensus’ private investment is supposed to be ‘good’ while state investment is supposed to be ‘bad’. The facts show the exact opposite trend is occurring. Rapidly rising state investment is associated with high economic growth (China and India): reliance solely on private investment is associated with low growth (US, EU and Japan).

Following the method of ‘seek truth from facts’ this article will first outline the trends in the global economy which must be explained and then analyse their causes.

China and India’s rapid growth

In 2015 China’s per capita GDP growth was 6.4% and India’s 6.3% on World Bank data. These are easily the fastest growth rates for any major economies. They also propel the most rapid rates of growth of household and total consumption. In particular, both China and India are growing far more rapidly than the ‘Western’ economies – in 2015 the EU’s per capita GDP growth was only 1.7%, the US 1.6%, and Japan’s 0.6%. Data for 2016 to date shows the same pattern of rapid growth in China and India and slow growth in the US, EU and Japan – as shown below.

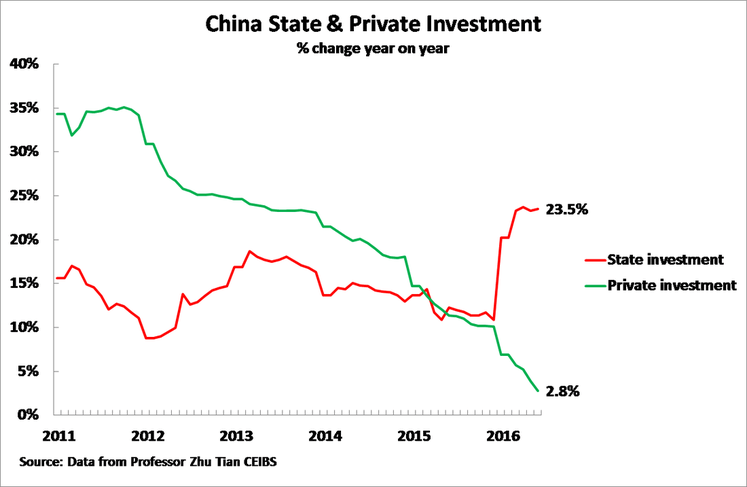

Turning to the macro-economic pattern of development in China and India, in China up to June 2016 the year on year growth of state-owned fixed-asset investment growth was 23.5% but private fixed asset investment growth declined to 2.8% – see Figure 1 which charts data kindly supplied by Professor Zhu Tian of CEIBS.

Naturally this is the overall pattern in China. In China’s ‘continental’ scale economy in some regions different patterns develop. For example, as Professor Yang JIanwen of the Shanghai Academy of Social Science has pointed out, Shanghai has promoted diversified ownership with many state companies listing to become shareholding companies. This is reflected in Shanghai in the year to June purely state investment fell by 11.0%, purely private investment fell by 5.1% but investment outside the pure state sector rose by 15.0% primarily due to a 30.0% increase in investment by joint stock companies with both private and state shareholders. But China’s overall pattern of a strong increase in state investment with only slowly rising private investment is clear from the national trends.

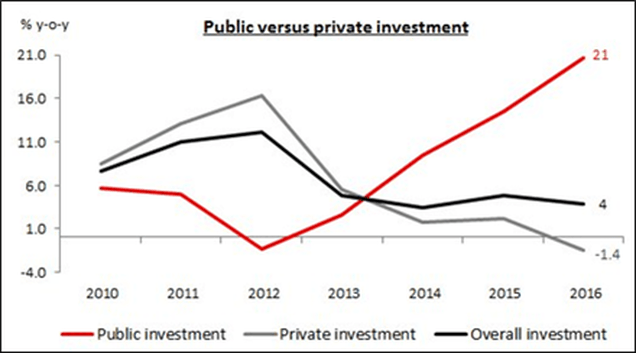

India, the other rapidly growing major economy, shows the same pattern as China. The analysis by Pranjul Bhandari, Chief India Economist of HSBC on 22 July, noted that on the latest data the year on year increase of India’s state investment was 21% while India’s private investment actually fell by 1.4% – see Figure 2.

In summary, the world’s two most rapidly major growing economies, China and India, are both being driven by rapidly rising state investment while private investment shows very low growth or it is even falling.

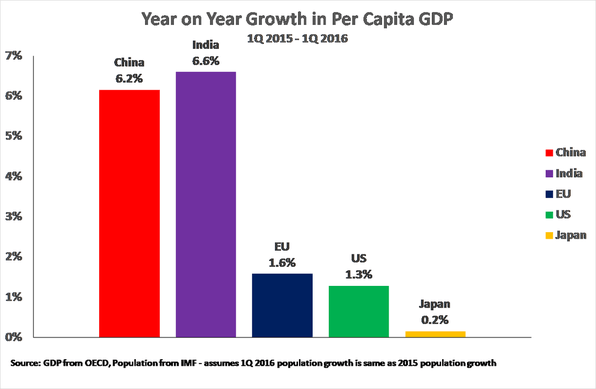

In contrast to China and India the Western economies are experiencing very slow growth. Figure 3 shows that up to the latest internationally comparable data, for the 1st quarter of 2016, per capita GDP growth was 6.2% in China, 6.6% in India but only 1.6% in the EU, 1.3% in the US and 0.2% in Japan – data for the 2ndquarter of 2016 shows continuation of the same growth rate in China while per capita growth in the US fell to 0.4%. That is, from the 2nd quarter of 2015 to 2ndquarter 2016 China’s per capita GDP rose over 14 times as fast as the US.

The vast growth outperformance by China and India compared to the Western economies is evident.

Low state investment in the West

If it may therefore be seen clearly that China and India’s pattern of high growth is associated with a rapid growth of state investment. What, therefore, is the pattern in the slow growing Western economies? As the best performing major Western economy is the US, which also publishes the most up to date data for state and private investment, this may be taken as the case study.

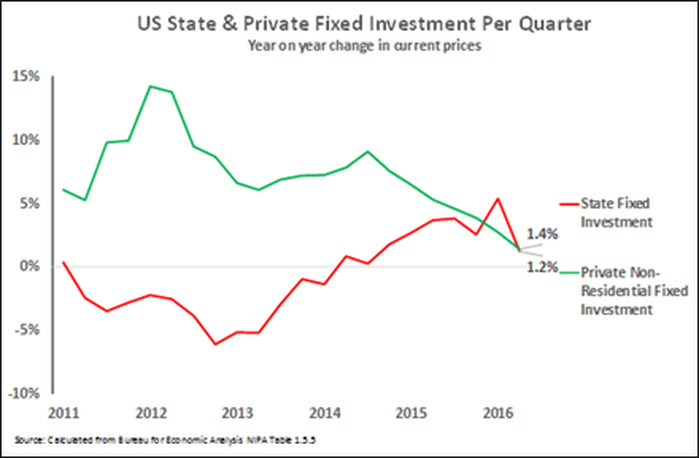

To allow a comparison with China the US data for state and private investment in current price terms is shown in Figure 5. This shows that the year on year growth of US private investment is also low as in China and India – a 2.4% increase to the 1st quarter of 2016. The growth rate of US private investment has also been steadily falling. But whereas in China and India the low growth rate of private investment is balanced by rapid growth rates of state investment of over 20% in the US the increase in state investment in the year to 2Q 2016 is only 1.2%. The US also publishes private and state investment data in inflation adjusted prices but this shows the same depressed trend – US private fixed investment in inflation adjusted prices rising 0.3% in the year to the 1st quarter of 2016 and state investment rising 0.8%. In short, unlike China and India, the US has not increased state investment to compensate for falling private investment.

The correlation between rapid growth of state investment and fast economic growth in China and India, and slower growth of state investment and slow economic growth in the US in the last period is therefore factually clear.

The role of state investment

Establishing causation in this correlation between rapid growth of state investment and fast economic growth, and reliance on private investment and low economic growth, is clear. It is in any case implausible that it is rapid economic growth which is leading to high levels of state investment in China and India, and low economic growth leading to low levels of state investment in the US. State investment is directly under the control of the governments and not subject to diffuse market forces. Both the Chinese and Indian government have made clear that they have deliberately taken the decision to increase state investment in order to stimulate economic growth, while the US is ideologically opposed to state investment.

China, in the early part of this year, deliberately stepped up its level of state investment in several programmes – particularly in infrastructure. By May the infrastructure investment action plan included 303 projects covering railways, highways, waterways, airports and urban rail transit, with 131 projects in 2016, 92 projects in 2017 and 80 projects in 2018. In late 2015-early 2016 China’s economy had been slowing and the rapid build-up of state investment was not a response to excessive strain caused by rapid GDP growth. As is well known it was a deliberate measure to stabilise the economy and prevent downturn.

In India the Modi government has appointed as its chief economic adviser a specialist on China’s economy – Arvind Subramanian, formerly of the Peterson Institute for International Economics and author of Eclipse: Living in the Shadow of China’s Economic Dominance. Immediately on Subramanian assuming his position in October 2014 he made clear that he saw state investment as the key to India’s growth. Subramanian was explicitly supported in this by India’s Finance Minister Arun Jaitley. This was then supported by a series of reports by top Indian economic thinkers. For example the Thought Arbitrage Research Institute issued the report ‘India Development Pathways 2040.’ Those contributing to its polices included former Planning Commission members Pronab Sen and Saumitra Chaudhari, former chief economic advisor Ashok Lahiri, former finance secretary C M Vasudev, former Finance Commission member D K Srivastava, Partha Chatterjee and George Matthew, among others. The report concluded: ‘Public investment will be the main driver of growth… At present, infrastructure spending is about six per cent of the gross domestic product (GDP), which needs to be increased to nine per cent to make a (yearly) growth rate of eight per cent sustainable over a long term.’ The rapid increase in India’s state investment reflected in the data is therefore an entirely conscious and deliberate policy pursued by the Indian government – the causal factor in the economic growth.

In the US however its ideology is that “state=bad’ and “private=good”. Therefore today the US rejects significant state investment on ideological grounds and also does not possess the structures, a major state sector of the economy, which is capable of delivering a rapid build-up of state investment. The way this false ideology and economic structure has severely hampered the US recovery from the international financial crisis is analysed in detail in my book 一盘大棋?(The Great Chess Game?). The US, of course, has sought to persuade other economies to adopt this policy of ‘state bad, private good’ through the Washington Consensus.

Trends in smaller economies

While China and India are easily the most important examples, because they are major economies, it is also clear that policies of state investment have achieved notably success in other economies as an increasing number of economists point out. As Professor of International Political Economy at Harvard University Dani Rodrik noted:

‘In Africa, Ethiopia is the most astounding success story of the last decade. Its economy has grown at an average annual rate exceeding 10% since 2004, which has translated into significant poverty reduction and improved health outcomes. The country is resource-poor and did not benefit from commodity booms, unlike many of its continental peers. Nor did economic liberalization and structural reforms of the type typically recommended by the World Bank and other donors play much of a role.

‘Rapid growth was the result, instead, of a massive increase in public investment, from 5% of GDP in the early 1990s to 19% in 2011 – the third highest rate in the world. The Ethiopian government went on a spending spree, building roads, railways, power plants, and an agricultural extension system that significantly enhanced productivity in rural areas, where most of the poor reside. Expenditures were financed partly by foreign aid and partly by heterodox policies (such as financial repression) that channeled private saving to the government.’

And regarding the Latin American continent:

‘Turning to Latin America, Bolivia is one of the rare mineral exporters that has managed to avoid others’ fate in the current commodity-price downturn. Annual GDP growth is expected to remain above 4% in 2015, in a region where overall output is shrinking (by 0.3%, according to the International Monetary Fund’s latest projections). Much of that has to do with public investment, which President Evo Morales regards as the engine of the Bolivian economy. From 2005 to 2014, total public investment has more than doubled relative to national income, from 6% to 13%, and the government intends to push the ratio even higher in coming years.’

Relation to China’s ‘new normal’

Turning to the interrelation of these trends with the ‘new normal’ in China it is well known that a key feature of the ‘new normal’ is that growth or foreseeable future period will be lower than the 9-10% annual growth rates seen for several decades after 1978 and which allowed the setting of an annual growth rate target of 8%. Part of the reason for this is the extremely slow growth of the international economy. This global ‘new normal’ was accurately described by IMF Managing Director Christine Lagarde as a ‘new mediocre’.

This slowdown in China is far less severe than in the advanced Western economies. In the year to the 1st quarter of 2016 China’s growth in per capita GDP at 6.2% was almost four times as rapid as the EU, almost five times as rapid as the US, and more than 20 times faster than Japan. Over the entire period 2007-2015 annual average per capita GDP growth in the US was only 0.5%, in Japan 0.2%, and in the EU 0.1%.

There is no doubt as to the reason for this extremely slowing growth in the Western economies. It was due to the extremely low rate of growth of fixed investment. Indeed, by 2015 the level of fixed investment in the advanced economies as a whole, the OECD region, was still below its level in 2007! The reason for this, as analysed in the case of the US, was that state investment failed to rise rapidly in order to compensate for stagnation or a falling rate of growth of private investment. In contrast China and India, by rapidly raising state investment, were able to achieve far higher growth rates.

The role of state investment in both China’s and the global ‘new normal’ is therefore clear.

Conclusions

The facts on the growth patterns in the ‘new normal’ of the global economy are therefore clear.

- The major economies with high rates of growth of state investment (China, India) have high rates of economic growth.

- The major economies with low growth rates of state investment, such as the US, have low rates of economic growth.

These trends also show why India has recently achieved growth acceleration and major economic success. India has broken with the ‘Washington Consensus’ of ‘state bad, private good’ to use state investment as the driving force of its economic development. It is not by accident that India appointed a China specialist as its chief economic adviser and its state investment policies have moved towards China’s pattern of development.

These global facts have clear implications for China’s economic policy and debates on it.

- International comparisons show it is clearly correct for China to have undertaken a policy of increased and targeted state investment.

- A policy relying purely on private investment is extremely unlikely to be unsuccessful as the experience of the US, Japan and EU confirms.

This economic reality is naturally is not a reason for not stimulating private investment – the most fundamental reasons for the decline in private investment have been dealt with by the present author elsewhere. However, the global trends analysed show clearly that state investment will have to play a key role in China’s economic development in the current period.

Global factual trends therefore show clearly that as President Xi Jinping rightly put it in an earlier economic discussion, for economic success China requires both the ‘invisible hand’ and the ‘visible hand’. This is counterposed to the ‘state bad, private good’ dogma which as has been shown is doing great damage in the West.

Naturally the global reality that state investment is a key factor in the present international ‘new normal’ is anathema to advocates for the ‘Washington Consensus’, i.e neo-liberalism. It is for this reason that neo-liberals dislike discussion of global economic facts and instead prefer utilisation of stereotyped phrases unrelated to reality.

The reason that these neo-liberal/Washington Consensus dogmas are out of touch with reality is that they are false not merely in relation to the facts of the development of the global economy but also in relation to economic theory. Analysis of these fundamental errors in economic theory would, however, require a separate article. For the present establishing that their dogmas have no relation to the facts will suffice.

China’s economic policy however is not about running a university class but about guiding the world’s second largest economy on which the fate of 1.3 billion people depends. The adoption by China of theoretically false economic positions such as ‘state bad, private good’ would under all circumstances be damaging. But in present global conditions, for reasons analysed in this article, the damage done is likely to be particularly rapid and severe.

Related articles

Key lessons from the failure of the US and success of China’s economic stimulus programmes

Why Chinese neo-liberals are forced to falsify world history

Why the US not China threatens world peace

China and US relations in Latin America